Montreal commercial real estate market update – Q1 2026

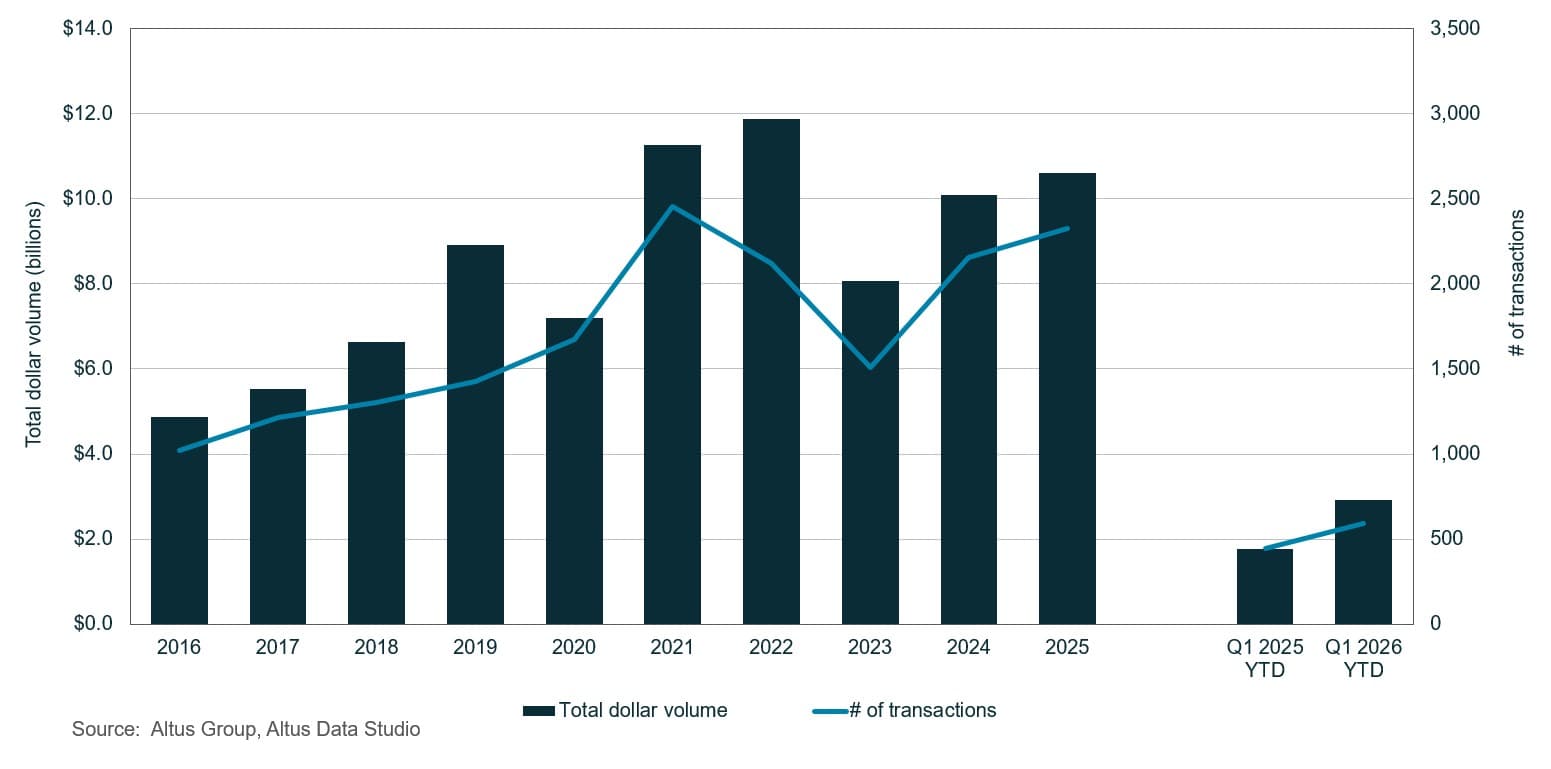

The Montreal commercial real estate market started the year with a total investment volume of $2.9 billion, a notable 65% year-over-year increase.

Key highlights:

Source: Altus Data Studio market data and analysis

By the close of the first quarter, Montreal reported a 65% year-over-year improvement in overall investment activity, with $2.9 billion in dollar volume transacted

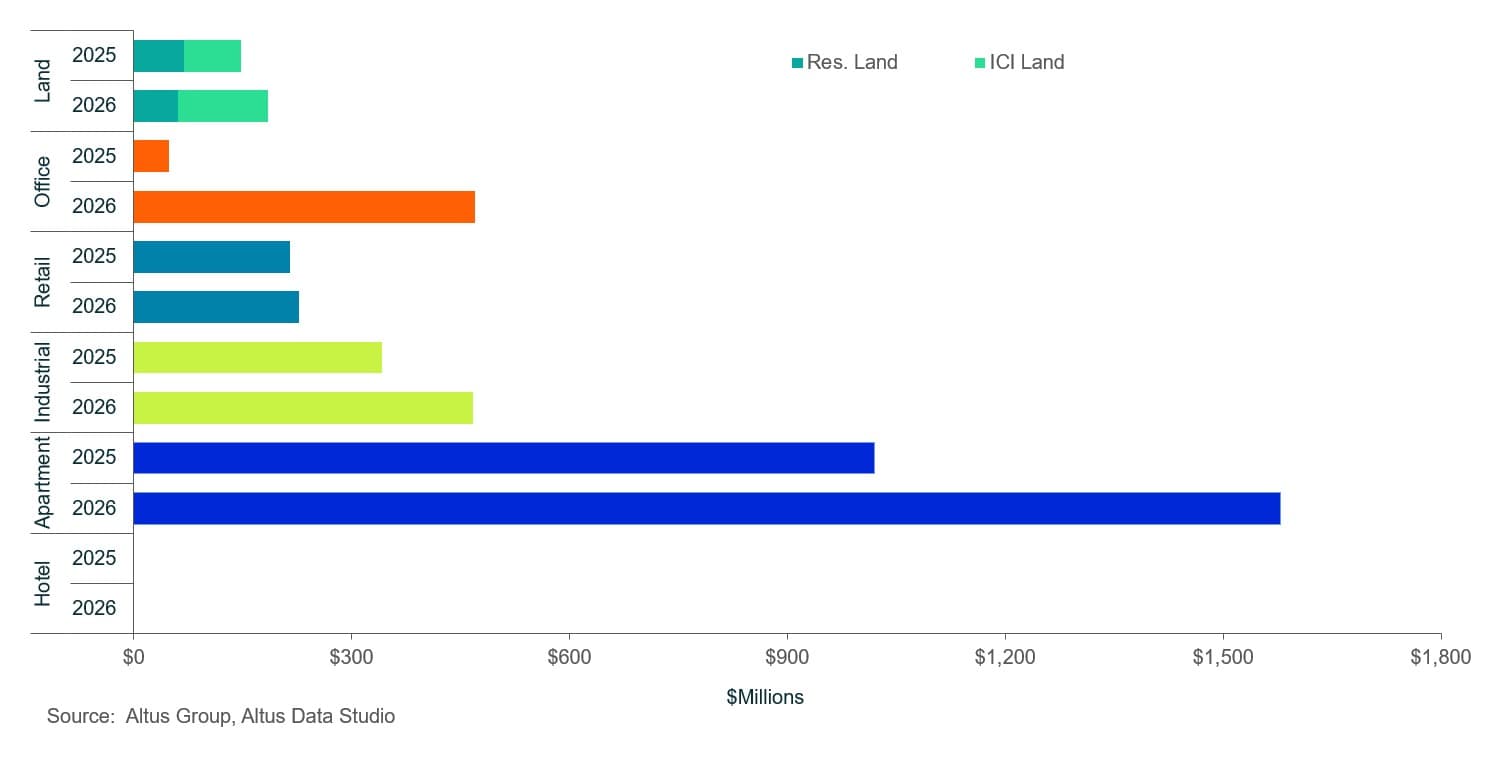

The multi-family sector demonstrated an upward growth trajectory, with investment volume up 55% year-over-year to $1.6 billion, comprising over half of the market’s total transaction volume

The industrial sector saw nascent signs of a pick-up, recording $467 million in dollar volume transacted, a 36% year-over-year increase

The retail sector saw a slight moderation with $227 million in dollar volume transacted, representing a modest 6% year-over-year increase

The office sector saw a significant increase, recording $470 million in dollar volume transacted, representing an astonishing 864% year-over-year increase

The land sector recorded nearly $185 million in dollar volume transacted, marking a 25% increase, the ICI sub-sector recorded $125 million in dollar volume transacted, while the residential land sub-sector recorded $60 million, up 58% and down 13% year-over-year, respectively

In the first quarter of 2026, Montreal saw strong investment activity, with volumes up 65% year-over-year

The Montreal commercial real estate market demonstrated notable resilience during the first quarter of 2026. Based on data from Altus Data Studio, total investment volume surged by 65% year-over-year to $2.9 billion. This robust performance followed a period of intensive recalibration in 2025 and occurred despite a complex global and domestic backdrop.

Figure 1: Montreal property transactions - All sectors by year

Domestic monetary policy continued to stabilize through early 2026. On March 18, 2026, the Bank of Canada (BoC) maintained its target for the overnight rate at 2.25%, marking the third consecutive hold. This decision signalled that while the central bank remained vigilant against commodity-driven inflationary pressures, the current rate was deemed appropriate to support a modest recovery in domestic demand.

However, this environment was increasingly tested by a softening local labour market. While the unemployment rate sat at 6.1% at the start of the quarter, the trajectory began to shift as the period progressed. By the close of March, the Montreal unemployment rate rose to 6.6%, indicating emerging employment headwinds. This increase was largely driven by a widening gap between labour supply and a slowdown in sectoral hiring, contributing to a more cautious outlook for the remainder of the 2026 calendar year.

In response to these conditions, investor sentiment in Montreal shifted toward a disciplined strategy of capital preservation, with a clear preference for defensive asset classes such as multi-family and food-anchored retail. Property owners prioritized balance sheet management through strategic refinancing, while most developers remained focused on intensifying existing sites rather than pursuing speculative new construction. Ultimately, the quarter was characterized by a transition from the volatility of previous years toward a period of calculated growth, as stakeholders gained confidence in the stability of the long-term neutral interest rate.

Multi-family investment activity

The multi-family sector solidified its position as a cornerstone of the Montreal commercial real estate market during the opening quarter of 2026. Accounting for 54% of total transactional activity, the asset class facilitated nearly $1.6 billion in investment volume, a substantial 55% increase year-over-year. This performance underscored the region’s unique demographic profile, characterized by a high proportion of lifelong renters, which maintained robust fundamental demand despite the broader headwinds affecting other major Canadian markets.

While the Island of Montreal sustained its historical dominance by securing $1.1 billion in capital inflows, the quarter was increasingly defined by a strategic expansion toward the peripheral submarkets. The Longueuil region recorded the most significant growth, with transaction volume surging by 394% year-over-year to $222 million. Investors were primarily drawn to the South Shore’s proximity to expanding transit infrastructure, which enhanced connectivity to the downtown core. This heightened demand was further supported by a lower cost of entry relative to the Island and a burgeoning demographic of young professionals seeking high-quality rental housing in well-integrated suburban hubs.

The political landscape further bolstered investor confidence following the election of Mayor Soraya Martinez Ferrada, whose administration implemented a pro-growth housing agenda. By prioritizing the deregulation of outdated zoning restrictions and authorizing the transfer of underutilized municipal land to private developers, the Mayor provided a decisive impetus to the rental sector. This commitment was reinforced by the strategic allocation of $30 million for subsidized land access, complemented by an additional $50 million in earmarked infrastructure funding. These fiscal measures effectively incentivized large-scale residential construction, signalling a favourable long-term outlook for the city’s housing supply.

Office investment activity

The Montreal office sector reported $470 million in dollar volume transacted in the first quarter of 2026. The resulting 864% year-over-year increase, while still significant, should be viewed in light of last year’s quarter being the third lowest on record. This resurgence in leasing activity was primarily driven by the widespread implementation of rigorous return-to-office mandates by major corporations and a definitive “flight-to-quality” investment strategy. These variables collectively funnelled investor appetite towards premium, strategically located Class AAA assets, which increasingly served as the primary anchor for the sector’s broader recovery phase.

The renewed emphasis on well-amenitized physical environments resulted in a notable tightening within the Class A market segment. According to the latest Altus Group Canadian Office Market Update, Montreal’s office availability rate contracted by 130 basis points to 16.4%. Specifically, Class A availability registered a decline of 210 bps year-over-year, settling at 14.7%. Meanwhile, Class B assets exhibited more marginal improvements, with availability receding by 90 bps to 18.5%. This discrepancy underscored a deepening bifurcation within the office market, as aging inventory failed to satisfy the sophisticated amenity and infrastructure requirements of modern corporate tenants.

The complete halt in new office completions further impacted the market’s structural balance. The regional development pipeline remained entirely stagnant, with no future office projects initiated, as the prevailing trend of converting or repositioning existing assets discouraged speculative new construction. This lack of incoming supply was expected to function as a primary driver for continued availability rate compression throughout 2026. As high-quality Class A inventory was increasingly absorbed by organizations prioritizing centralized, high-performance corporate hubs, the scarcity of premium space exerted additional upward pressure on the competitive landscape.

Industrial investment activity

The industrial sector showed nascent signs of a pick-up during the first quarter of 2026, with investment volume increasing 36% year-over-year to over $466 million. However, this uptick followed a sustained period of volatility as stakeholders adjusted to a more conservative economic environment and fluctuating trade dynamics. According to the latest Altus Group Canadian Industrial Market Update, Montreal’s availability rate reached 8.5%, representing a year-over-year increase of 90 bps. The market notably endured eight consecutive quarters of negative net absorption before a brief transition into positive territory in the fourth quarter of 2025, followed by another slight contraction in the first quarter of 2026.

Location was the main factor driving changes across the region’s industrial landscape. Assets situated on the Island of Montreal were largely defined by antiquated infrastructure, characterized by insufficient clear heights and prohibitive operation expenses, which failed to align with modern logistics and fulfillment standards. In contrast, the South Shore established itself as a premier destination for next-generation distribution centres, providing superior land tracts and state-of-the-art technical specifications. Amidst these shifting dynamics, net asking rents remained stagnant, hovering within the $13 to $14 per square foot range for 12 consecutive quarters.

Investor sentiment remained cautious but opportunistic, with a primary focus on risk mitigation. While capital began to return to the sector, many institutional players stayed on the sidelines, waiting for clearer signals regarding interest rate policies and the potential impact of shifting geopolitical uncertainties. The first quarter concluded with the delivery of three industrial buildings totalling nearly 372,000 square feet, though 63% of that space remained uncommitted at the time of completion. The development pipeline consisted of 13 buildings under construction, representing 2.6 million square feet. Notably, 56% of this future supply remained unleased. Ultimately, a substantive recovery in industrial demand remained contingent upon clearer geopolitical trade signals and a resurgence in consumer spending, ensuring that a corresponding increase matches the high volume of incoming supply in logistical throughput.

Retail investment activity

The retail sector sustained the momentum established during 2025, with the first quarter of 2026 reporting a total transaction volume of $227 million. While this figure represented a 6% year-over-year increase, it signalled a notable moderation compared to the record highs achieved in the final quarter of 2025, primarily due to the landmark $565 million acquisition of Promenades St-Bruno in the previous period. This cooling suggested that investors continued to be more selective, prioritizing long-term stability over aggressive expansion.

Food-anchored retail strips remained the primary choice for investors, as a cautious consumer base focused on essential goods and services, which kept demand for necessity-based retail resilient. Furthermore, the asset class’s efficacy as an inflation hedge resulted in an acute inventory shortage across the market. Property owners increasingly retained these high-performing assets rather than bringing them to market. Simultaneously, restrictive lending environments and the elevated cost of capital severely constrained the feasibility of new development projects.

Consequently, near-term investment activity remained largely suppressed by a lack of available product and the persistence of high financing costs. Strategic focus shifted toward the intensification of existing sites, with owners exploring the integration of residential components into suburban shopping centres to create high-density, mixed-use hubs. This strategy served to maximize land value while establishing a captive consumer base, effectively safeguarding the long-term viability of these retail assets.

Land investment activity

The land sector in Montreal, encompassing both residential and ICI land, experienced a 25% year-over-year increase, with transaction volume for the period reaching nearly $185 million. However, this growth followed several years of persistent decline, suggesting that the statistical improvement may be slightly overstated when viewed in the broader context. A conservative investment climate and a notable deceleration in development activity remained prevalent throughout the region, as stakeholders continuously assessed shifting economic variables and the impact of elevated borrowing costs on project viability.

A granular analysis of the sector revealed that the ICI land segment served as the primary catalyst for the uptick in activity. Transaction volume within the ICI sub-sector totalled nearly $125 million, representing a substantial 58% year-over-year expansion. This surge was likely driven by strategic acquisitions for future logistics and specialized industrial use, as firms sought to secure limited serviced acreage in anticipation of the long-term supply shortages.

Conversely, the residential land sector experienced a contraction in activity, reporting $60 million in dollar volume, a 13% year-over-year decrease. This downturn underscored a deliberate shift in developer behaviour toward highly selective land acquisition and rigorous due diligence. The reduction in residential land acquisition for the past several years functioned as a clear indicator of a sector-wide transition toward risk mitigation. Developers and investors prioritized a defensive posture, re-evaluating long-term pipeline strategies in direct response to evolving market fundamentals. This conservative approach reflected a broader trend of capital preservation, as stakeholders remained hesitant to commit to large-scale residential projects without a clearer trajectory for future exit values and absorption rates.

Figure 2: Property transactions by total by asset class YTD (Q1 2025 vs Q1 2026)

Notable Montreal property transactions

The following are the notable transactions for the Q1 2026 Montreal commercial real estate market update:

Tour Deloitte, Montreal (Ville-Marie) – Office

Marking the largest office transaction nationally during the first quarter, Cadillac Fairview (CF) sold Tour Deloitte to German investor DekaBank for $279 million. Completed in 2015, Tour Deloitte (1115 Saint-Antoine Street West) boasts over 513,000 square feet of office space on 26 floors. The building was directly connected to Montreal’s RÉSO underground pedestrian network and was fully leased at the time of sale.

Later in the first quarter, CF also sold the adjacent Windsor Station (1111 Saint-Antoine Street West), a fifteen-storey, 326,000 square foot office building. This property was also directly connected to the RÉSO and has an additional 37% ownership stake in the Bell Centre underground parking lot. CF also traded the building to Laurier Capital & Society Développement Immobilier for $49.6M. Another notable office disposition by CF was the $140 million sale of the Yonge Corporate Centre in Toronto (North York), Ontario.

Le Sommet, Montreal (Ville-Marie) - Apartment

Hazelview Investments sold this 16-storey, 291-unit residential apartment building to Priveda Capital for a total consideration of $90.5 million. Hazelview had previously acquired the property in May 2019 for $82 million. The highly amenitized building features an outdoor pool, gym, and rooftop terrace. Later the same month, Hazelview also disposed of the 16-storey, 91-unit building at 440-450 Sherbrooke Street East for $25.75 million.

2501 Trans-Canada Highway, Montreal (Pointe-Claire) - Industrial

French investment firm Alderan acquired 2501 Trans-Canada Highway from Montreal-based developer Brasswater for $76.8 million. The fully occupied, 274,044 square foot manufacturing and distribution centre was situated on a 15-acre site, on the north service road of Highway 40. The building was originally constructed in 1962 and features 27-foot clear heights, 14 truck-level doors, and 10 drive-in doors. Brasswater had acquired the property on June 7, 2023, for a total consideration of $60 million, representing a price of $219 per square foot.

Alderan further strengthened its investment presence in Canada through a land acquisition for the development of Club Med Tremblant. Scheduled to open in December 2028, the new resort was designed to accommodate as many as 400 rooms. Alderan’s increasing investment activity in Quebec signals confidence in the long-term regional market outlook.

Faubourg Bois-Franc, Montreal (Saint-Laurent) - Retail

Located just west of the new Bois-Franc REM station, this six-building retail centre was acquired by Fiera Real Estate for $44.5 million. The plaza was constructed between 2015 and 2020 and was 95% occupied at the time of sale. Anchored by IGA and Jean-Coutu, the property contained nearly 134,000 square feet of space.

This retail asset was well-positioned as a local shopping hub for several transit-oriented developments that were in progress. This includes Montoni’s 300-unit Chapitre Bois-Franc, Montclair’s 450-unit Aura sur le Square and Jadco’s 525-unit Equinoxe Bois-Franc, all of which were located in the immediate vicinity. Three of the buildings within the Faubourg Bois-Franc were situated on the street level of six-storey condo buildings. These three buildings contained approximately 161 residential condo units and were serviced by underground parking.

Looking ahead

As the Montreal commercial real estate market moves further into 2026, the prevailing narrative has shifted from one of reactive uncertainty to a phase of calculated acceleration. Following a robust opening quarter, the Montreal market is poised for a gradual increase in transactional velocity. This conviction is increasingly underpinned by the return of major institutional groups, whose substantial liquidity and renewed conviction are expected to shift the buyer landscape back toward its historical equilibrium. However, this resurgence is occurring amid complex structural transitions.

A stabilized monetary environment has provided a much-needed anchor for the market. With the BoC holding the overnight rate, the clarity regarding the cost of capital has allowed investors to move past the “wait-and-see” approach that defined 2025. This predictability has refined underwriting standards, though investor sentiment remains firmly anchored in a disciplined “flight-to-quality.” While liquidity is returning, capital is being deployed with high selectivity, prioritizing assets with strong income profiles and resilient locations to hedge against shifting demographic and economic uncertainties.

The second half of 2026 introduces specific geopolitical and demographic crosscurrents that will require a defensive posture. Most notably, the mandatory joint review of CUSMA serves as a strategic wildcard, likely tempering speculative activity until trade conditions are clarified. Furthermore, as national population growth trends shift, Montreal’s relative resilience continued to offer a competitive advantage for institutional portfolios. Ultimately, the outlook is one of measured stabilization. While the re-entry of institutional players signals a recovery in market participation, the focus remains on risk mitigation and capital preservation as stakeholders navigate a period of significant economic recalibration.

Want to be notified of our new and relevant CRE content, articles and events?

Disclaimer

This publication has been prepared for general guidance on matters of interest only and does not constitute professional advice or services of Altus Group, its affiliates and its related entities (collectively “Altus Group”). You should not act upon the information contained in this publication without obtaining specific professional advice.

A number of factors may influence the performance of the commercial real estate market, including regulatory conditions and economic factors such as interest rate fluctuations, inflation, changing investor sentiment, and shifts in tenant demand or occupancy trends. We strongly recommend that you consult with a qualified professional to assess how these and other market dynamics may impact your investment strategy, underwriting assumptions, asset valuations, and overall portfolio performance.

No representation or warranty (express or implied) is given as to the accuracy, completeness or reliability of the information contained in this publication, or the suitability of the information for a particular purpose. To the extent permitted by law, Altus Group does not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it. The distribution of this publication to you does not create, extend or revive a client relationship between Altus Group and you or any other person or entity. This publication, or any part thereof, may not be reproduced or distributed in any form for any purpose without the express written consent of Altus Group.

Authors

Jennifer Nhieu

Senior Research Analyst

Stephen Robinson

Team Lead, Market Research

Authors

Jennifer Nhieu

Senior Research Analyst

Stephen Robinson

Team Lead, Market Research

Resources

Latest insights