Key highlights

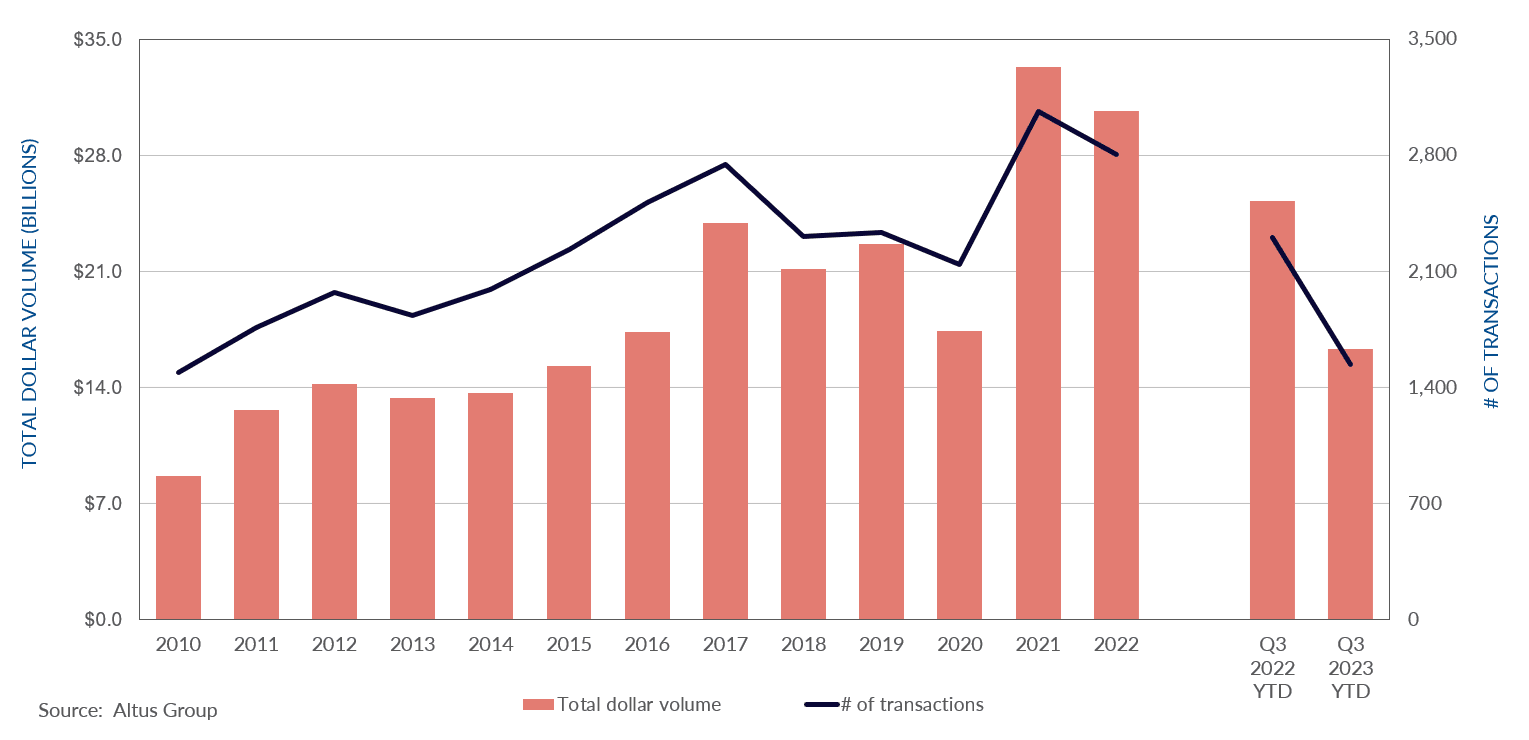

The Greater Toronto Area (GTA) market reported $16 billion in dollar volume through the first three quarters of 2023, a 35% decrease year-over-year

The only sector to experience growth was the hotel sector, primarily driven by the large-scale transaction of The Hazelton Hotel ($105 million) along with a few other hotel transactions by private investors

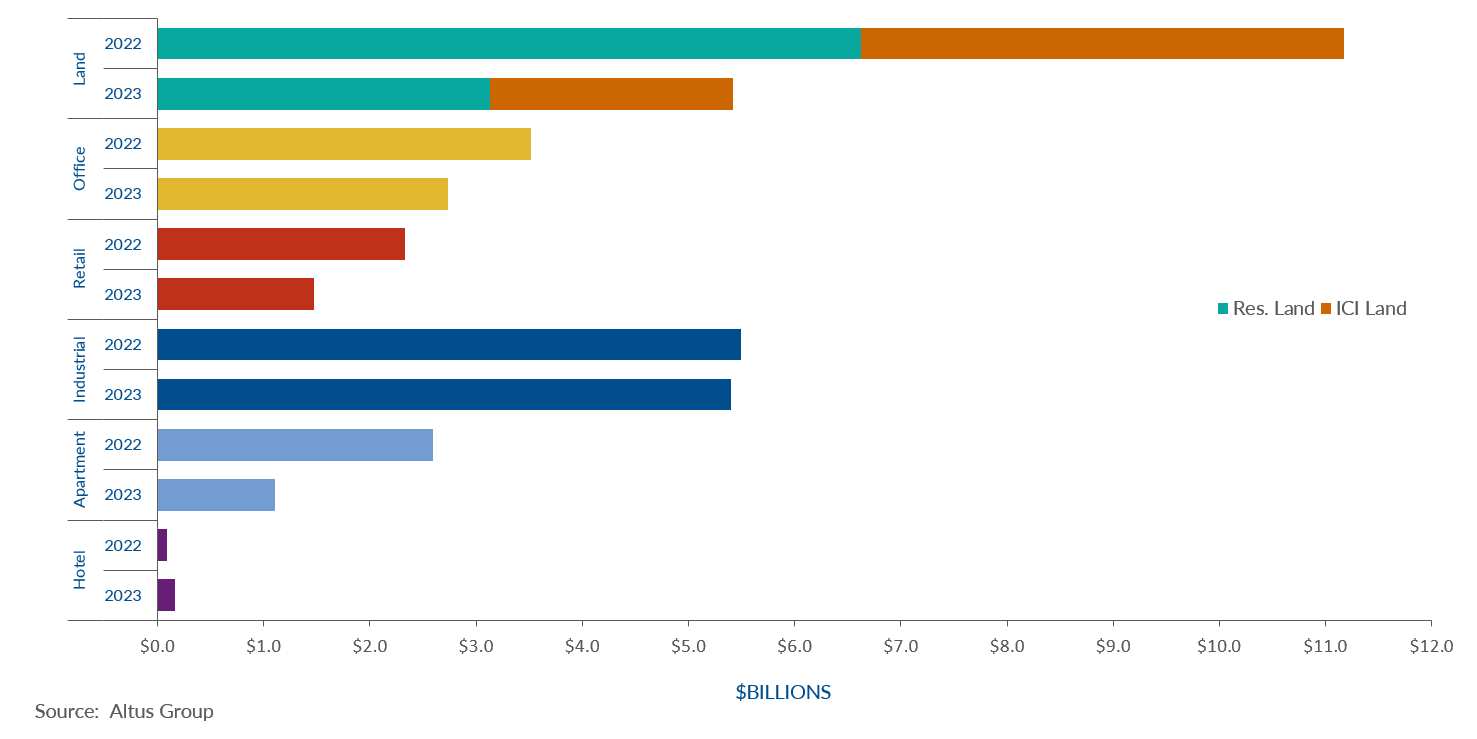

The industrial sector remained the strongest sector in the GTA, reporting $5.4 billion in dollar volume transacted, a minimal decrease of 2% year-over-year

The multi-family sector reported $1.1 billion in dollar volume transacted, a 57% decrease year-over-year

Office transactions continued to drop in Q3 2023, with only $2.7 billion in dollar volume transacted (a 22% decrease year-over-year), as uncertainty lingered and investors pivoted to more stable, low-risk areas of real estate

The retail sector reported $1.5 billion in transaction volume in Q3 2023, a 37% decrease year-over-year

Despite the slowdown in overall sales activity, investors remained committed to the industrial and multi-family sector in the GTA market

GTA market’s slowdown extends into Q3 2023, with transaction volume down 35%

The Greater Toronto Area (GTA) reported $16 billion in dollar volume through the first three quarters of 2023, a 35% decrease year-over-year. The lingering effects of higher interest rates and borrowing costs have contributed to the pullback in sales activity. The only sector to experience growth was the hotel sector, primarily driven by the large-scale transaction of The Hazelton Hotel ($105 million) along with a few other hotel transactions by private investors. The GTA continued to observe soaring demand for industrial assets and the number of industrial projects in the construction pipeline continued to increase to address the market's tight market conditions.

Figure 1 - GTA property transactions – All sectors by year

The industrial sector remained the strongest sector in the GTA, reporting $5.4 billion in dollar volume transacted, a minimal decrease of 2% year-over-year. Despite elevated interest rates, the GTA’s industrial sector has positioned itself for growth due to favourable market conditions and demand outpacing supply. According to Altus Group’s Q3 Canadian industrial market update, Toronto’s industrial availability rate increased to 2.6% but remained the lowest in Canada. Furthermore, the GTA saw approximately four million square feet of new supply enter the market, with over 60% pre-leased. In addition, over 16 million square feet of supply are under construction as the demand for distribution and warehousing facilities grows.

The multi-family sector reported $1.1 billion in dollar volume transacted, a 57% decrease year-over-year. The bid-ask gap between buyers and sellers, the tightening of lending practices from financial institutions, unmet demand for labour, and increased construction and material costs have resulted in a gradual pullback in activity. According to Altus Group’s most recent Investment Trends Survey, suburban multi-unit residential in the GTA market dropped ten spots to the 11th preferred location and property type combination in Q3 2023. However, population growth and the shortage of available rental units have contributed to an increase in the demand for purpose-built rentals. The long-term outlook for the sector remains favourable, as the asset class displayed resilience amidst volatile economic conditions.

Office transactions continued to drop in Q3 2023, with only $2.7 billion in dollar volume transacted (a 22% decrease year-over-year), as uncertainty lingered and investors pivoted to more stable, low-risk areas of real estate. As shared in Altus Group’s most recent Canadian office market update, office availability rates have flattened nationwide, with the GTA holding steady at 18.1%. The GTA has not introduced any new supply in Q3 2023. In addition, nearly 6.2 million square feet of office space is expected to enter the market, which will include class-A buildings located in the downtown core.

The retail sector reported $1.5 billion in transaction volume in Q3 2023, a 37% decrease year-over-year. As the hybrid work model has become a permanent fixture for many Canadian workplaces, people have spent more time at home and in their local neighbourhood. Altus Group’s latest Canadian Investment Trends Survey revealed that food-anchored retail strips emerged as the top preferred product type in Q3 2023. Grocery-anchored neighbourhood-level retail centres have drawn the attention of investors since the pandemic, for their resilience to economic uncertainty and the impact of e-commerce.

Figure 2 - GTA property transactions by asset class (YTD Q3 2022 vs YTD Q3 2023)

Despite the slowdown in overall sales activity, investors remained committed to the industrial and multi-family sector in the GTA. Moreover, while not all areas of retail real estate have bounced back since the pandemic, investors have displayed a greater interest in food-anchored retail. A gradual pullback in investment in the multi-family sector was observed as investors adjusted to higher financing costs. Furthermore, activity is expected to remain sluggish for the remainder of 2023, but the future outlook remains positive as the market is supported by strong underlying demographic and economic fundamentals.

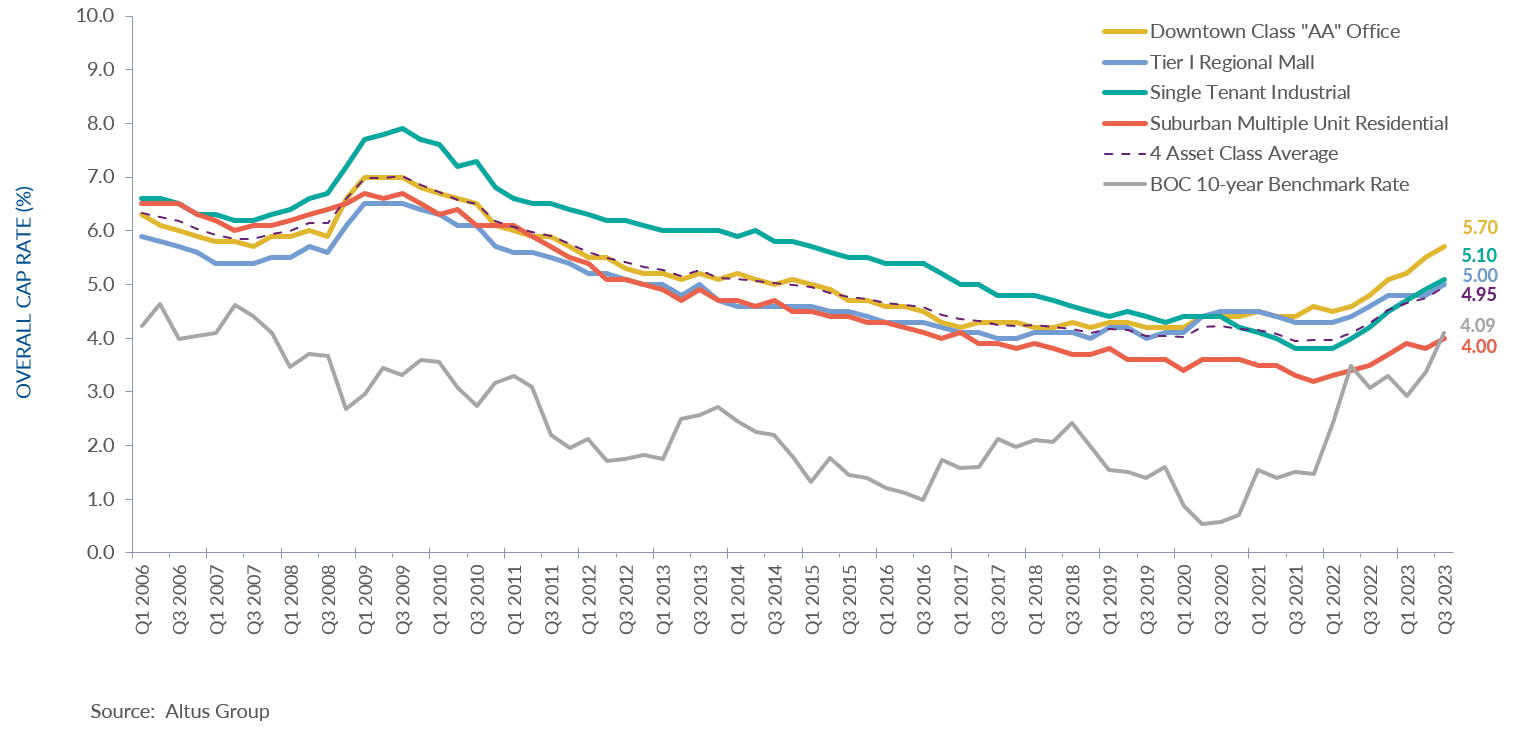

Figure 3 - GTA OCR trends across 4 benchmark asset classes

Notable transactions for Q3 2023

Atria I, II & III, North York – Office

Groupe Mach & Sarees Investments have partnered to acquire the three buildings that form the Atria Complex for $165 million, representing one of GTA’s highest dollar transactions within the quarter. With a total gross leasable area of 921,834 square feet, it is promoted as one of the largest office complexes on the edges of downtown Toronto, yet the price per square foot of $179 represents one of the lowest in the quarter for offices. While the purchasers are confident in the resurgence of in-person office work, the potential land value also factors into their investment strategy. A portion of the 14-acre land permits residential zoning, creating potential redevelopment opportunities. The vendors of this transaction, AIMCo and Dorsay Development Corp., originally acquired the complex in September 2005 for a total of $131 million.

King Street, Caledon – Residential Land

ARGO Development Corporation acquired this 44-acre site for $50 million, representing one of the largest residential land transactions in the quarter. The subject property was part of a six-property, 262-acre land assembly acquired over five years, totalling $166.3 million. Development applications for a master-planned community have been submitted on these lands, with the most recent proposal in May 2023 for the development of 580 single-detached dwellings, 1,695 units of various townhouse types, elementary schools, parks, as well as residential reserves on which future and separate applications will occur. This development is one of many upcoming residential developments in Peel Region by the Burlington-based developer.

250 Chrysler Drive, Brampton – Industrial

This 150,000-square-foot warehouse and distribution centre was purchased for $44 million in a joint venture between GIC and Dream Industrial REIT. The limited partnership had previously acquired Summit Industrial Income REIT for $5.9 billion in the first quarter of this year. The vendor on this property was BentallGreenOak, who had previously purchased the building in 2011 for $10.9 million. Sitting on nearly seven acres, the six-unit building was fully occupied at the time of sale by three tenants with in-place rents below current market levels.

30 Normandy Place, Oakville – Apartment

Halton Region acquired this 70-unit apartment for $16 million and forms a part of its assisted housing initiatives for low-income families. As units vacate and new applicants for assisted housing are placed into the apartment, Halton Region plans to transition 75% of units to deep subsidy with 25% of units at 80% of market rent. This will require the Region to subsidize operational and capital expenditures by 2028 to Halton Community Housing Corporation, which manages the apartment.

Authors

Jennifer Nhieu

Senior Research Analyst

Lucy Wu-Yu

Market Analyst

Authors

Jennifer Nhieu

Senior Research Analyst

Lucy Wu-Yu

Market Analyst

Resources

Latest insights